Okay, so you want to make your money work for you? Great decision! But hold on—before you start imagining yourself with a luxury car, big house, and a beachside holiday in Goa, let’s first figure out how to actually get there without turning your hair gray. 🧑🦳💸

The world of investing is like a big Indian wedding: it’s full of options, can be a little overwhelming, and you’ll find that everyone has an opinion. Don’t worry, we’ve got your back! Let’s dive into the different ways of investing—Indian style!

1. Stocks: The Dhol Tasha of Investment 🎉

If stocks were a wedding procession, they’d definitely be the dhol tasha. Loud, fast-paced, and definitely giving you a rush of excitement. One minute, you’re on a high, dancing to the beat, and the next, you’re stumbling over your feet.

- Pros: Stocks give you the potential to hit big, like buying the latest smartphone at a discount and selling it at a premium. 🚀📱

- Cons: They’re as unpredictable as the weather during monsoon season. You could either end up with a sweet profit or get drenched in losses. 🌧️

Tip: Always remember—stocks are like your cousin’s dance moves at the wedding: sometimes they surprise you, but they can also trip you up. Keep your eyes open!

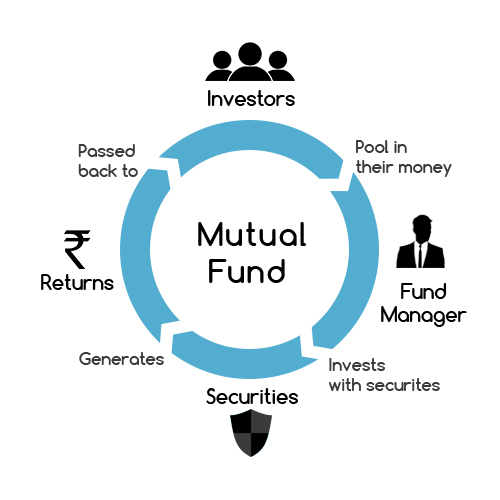

2. Mutual Funds: The Thali of Investment 🍽️

Mutual funds are like a delicious thali at a wedding—plenty of options in one plate. You’ve got your dal, rice, sabzi, and sweet dish, all mixed in together by a fund manager (or chef!). It’s a well-balanced choice, perfect for those who want to try a little bit of everything without the risk of overdoing it.

- Pros: Diversification, baby! It’s like having a small bite of everything—large, mid, and small-cap stocks. 🍚🍲

- Cons: You’ll have to pay the fund manager for mixing your plate, and sometimes, those extra charges can be like the added cost of the wedding buffet. 💸

Tip: Think of mutual funds as the "Safe Bet" for those who want to attend the party but don’t want to risk getting caught up in the drama. 😅

3. Real Estate: The Plot of Land You’ll Call ‘Home’ 🏠

If you’re looking for a “solid investment” that you can actually see and touch, real estate is your go-to. It’s like owning your own piece of land in a growing city like Pune or Gurgaon. It’s an investment that doesn’t come with surprise twists—unless, of course, you forget about property taxes. 😬

- Pros: You get to be a “landlord,” which is pretty cool. And if you’re renting it out, you can sip chai and get paid. ☕💰

- Cons: If things go wrong, like your tenant turning into a Bollywood villain, things can get messy. It’s like having to deal with an uncle who asks why you're still single at every family gathering. 🏠🧨

Tip: Real estate is for those who believe in ghar ki khushboo and long-term investments. But be prepared for some paperwork—it's like a wedding guest list that never ends! 📝

4. Gold: The Ancestral Investment 🏅

If you’re an Indian, gold is like the sasural ka taweez—it's passed down through generations, and it always has value. Whether it’s a shiny new gold coin or your grandmother's jewelry, gold has stood the test of time.

- Pros: Gold is always in demand, especially around festivals like Diwali. Plus, it’s as safe as your mom’s advice during a crisis. 🏅

- Cons: It's not exactly liquid—unlike your pocket money that you can spend on shopping whenever you want. 💍

Tip: If you like the idea of an asset that’ll sparkle forever (even when the stock market looks a little dull), gold is your friend.

5. Cryptocurrency: The Desi “Naya Trend” 💻

Ah, cryptocurrency—the new-age “Bitcoin” trend that even your cousin is talking about at family gatherings. It’s like the cool kid at school who is a little too unpredictable but still gets everyone’s attention.

- Pros: If you’re lucky, you could make money faster than a rickshaw ride during peak hours. 🚖💸

- Cons: It’s as volatile as a sudden power cut during your favorite TV show. One minute you're on top, and the next, you're left in the dark. ⚡

Tip: If you like taking risks and feel like you’ve got the guts to handle sudden rollercoaster-like swings, crypto’s the ride for you!

6. Fixed Deposits (FDs): The Comfort of Your Mother’s Cooking 🍲

, steady return with no drama, Fixed Deposits (FDs) are like your mom’s cooking—reliable, comforting, and steady. You put your money in, and you know it’ll grow at a fixed interest rate, just like the way the potatoes cook in your kitchen.

- Pros: It’s the safest bet! No wild ups and downs, no unnecessary excitement—just pure comfort. 🏦

- Cons: The returns are slower than a rickshaw on a rainy day, and your money is locked up for a while. ⏳

Tip: If you prefer peace of mind and want to build wealth slowly (like your favorite slow-cooked dal), FD is your go-to.