Financial Tips for First-Time Earners: A Fun Guide

Congrats on your first paycheck! Whether you’re feeling like a rockstar or an ATM, managing your money wisely now can set you up for a bright financial future. Here’s how to do it with a smile (and without eating instant noodles forever).

1. Budget Like a Boss

Think of a budget as your financial GPS—it keeps you from getting lost in the shopping mall. Start with the 50/30/20 rule:

- 50% for needs (rent, food, Wi-Fi—yes, Wi-Fi is a need).

- 30% for wants (new sneakers, Netflix, that fancy coffee).

- 20% for savings and investments (future you will thank you!).

2. Build an Emergency Fund

Life happens—like your phone deciding to swim in the sink. Save at least three months’ worth of expenses in an emergency fund. Pro tip: Keep this money in a separate, easily accessible account.

3. Avoid the Debt Trap

Credit cards are like dessert—great in moderation but dangerous in excess. Pay your bills on time and avoid borrowing for things you don’t need. Remember, debt is like a clingy ex—it’s hard to shake off.

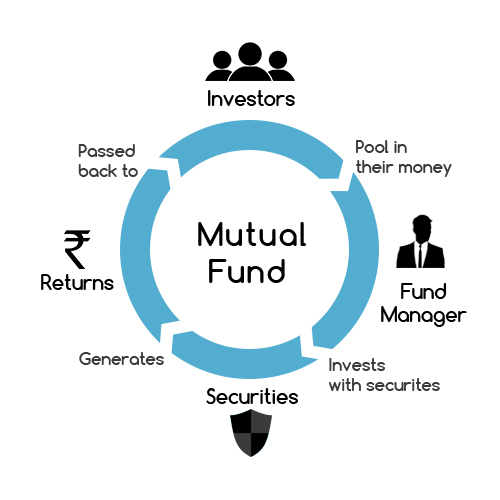

4. Start Investing Early

Investing is like planting a tree. The earlier you start, the sooner you’ll enjoy the shade. Explore options like mutual funds, SIPs, or even index funds. And no, gambling on stocks isn’t the same as investing!

5. Learn About Taxes

Welcome to adulthood, where taxes are as inevitable as wedding invites. Learn how to file your returns and explore ways to save on taxes through deductions and exemptions. Google "Section 80C" to start.

6. Don’t Forget Insurance

Insurance is your financial safety net. Get health insurance even if you think you’re invincible. And if you’re supporting your family, consider life insurance too.

7. Keep Learning

Money management is a lifelong skill. Read books, follow finance blogs, and maybe even attend a workshop. The more you know, the more confident you’ll be.

FAQs for First-Time Earners

Q: Should I save or invest first?

A: Start by building an emergency fund, then focus on investments.

Q: Is it okay to spend on luxuries?

A: Yes, as long as it fits within your budget. Treat yourself—but don’t overdo it.

Q: How can I learn about investing?

A: Start with beginner-friendly resources like books, blogs, or even YouTube videos. Practice with small amounts.